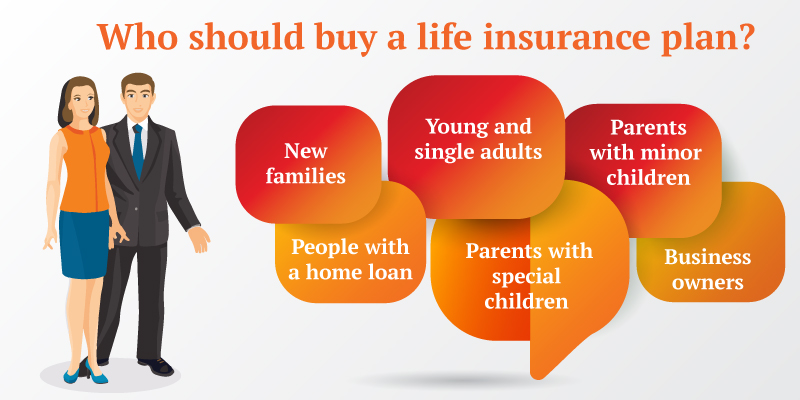

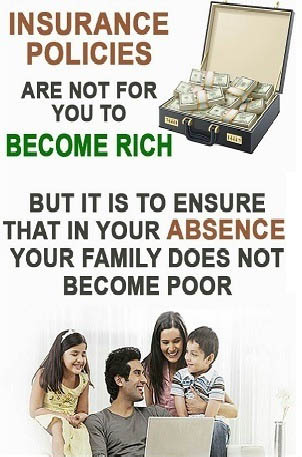

One of the most important things you can do as parents is to ensure the financial welfare of your children in the event of your death. Life insurance is the best way to be rest assured that your children will be taken care of if you die. Although we never like to think of that kind of thing happening, but it does. Under life insurance, the life of the individual is assured. This means that at the time of his/ her death, the family members receive an assured amount. Life insurance not only helps the survivors for their financial requirement after death of the earning member, but also helps in achieving financial goals during the lifetime. It also provides a tool of savings and tax planning.

One of the most important things you can do as parents is to ensure the financial welfare of your children in the event of your death. Life insurance is the best way to be rest assured that your children will be taken care of if you die. Although we never like to think of that kind of thing happening, but it does. Under life insurance, the life of the individual is assured. This means that at the time of his/ her death, the family members receive an assured amount. Life insurance not only helps the survivors for their financial requirement after death of the earning member, but also helps in achieving financial goals during the lifetime. It also provides a tool of savings and tax planning.